Select menu: Stats | Time Series | ARIMA Model Fitting

Fits an autoregressive integrated moving-average (ARIMA) model to time-series data. The series and results can be displayed graphically, and forecasts of future observations can be formed.

- After you have imported your data, from the menu select

Stats | Time Series | ARIMA Model Fitting. - Fill in the fields as required then click Run.

You can set additional Options then after running the analysis you can save the results by clicking Save.

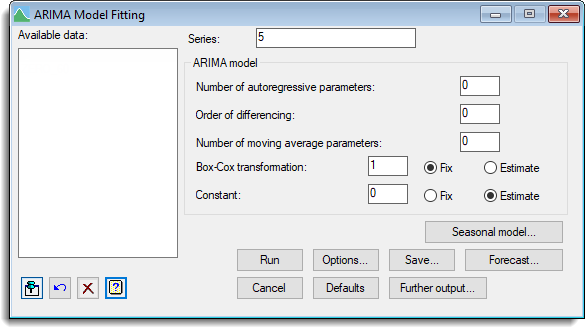

Available data

This lists variates that can be used as the Series data. Double-click a name to copy it to the Series field or type the name.

Series

Specifies a variate containing the time series data.

ARIMA model

Specifies the model to be fitted, using the Box-Jenkins ARIMA notation. You need to supply the orders for the model, that is, the number of parameters for the autoregressive and moving-average parts of the model, and the degree of differencing required. You can also specify whether the constant term should be fixed at a given value or estimated, and whether a Box-Cox transformation should be applied to the data before analysis using either a fixed value or estimating the optimal transformation. The default action is to fix the Box-Cox parameter to 1, i.e. no transformation.

Action Icons

| Pin | Controls whether to keep the dialog open when you click Run. When the pin is down |

|

| Restore | Restore names into edit fields and default settings. | |

| Clear | Clear all fields and list boxes. | |

| Help | Open the Help topic for this dialog. |

See also

- Options for controlling what statistics are displayed

- Seasonal Model for including seasonal components in the model

- Further Output for additional printing and plotting of results

- Save for saving the results from an ARIMA analysis

- Forecast for generating forecasts from the fitted model

- TSM directive for specifying ARIMA models

- TFIT directive for fitting ARIMA models